Published on

After peaking at a 40-year high in 2024, delivery of new multifamily units has tapered off. The volume of new deliveries fell from 695,000 units in 2024 to 531,000 units in 2025. In 2026, deliveries are projected to drop to 382,000 units.

But even as the construction pipeline has slowed down, supply has remained elevated, and moderating renter demand has failed to absorb the excess supply. This supply–demand mismatch has restrained rent growth and kept national multifamily vacancy hovering above 8 percent.

In this challenging environment for owners and operators, how long will the multifamily recovery take? The latest forecast and analysis from Apartments.com, powered by CoStar data, reveal what’s ahead. Let’s take a closer look at recent supply trends shaping the market.

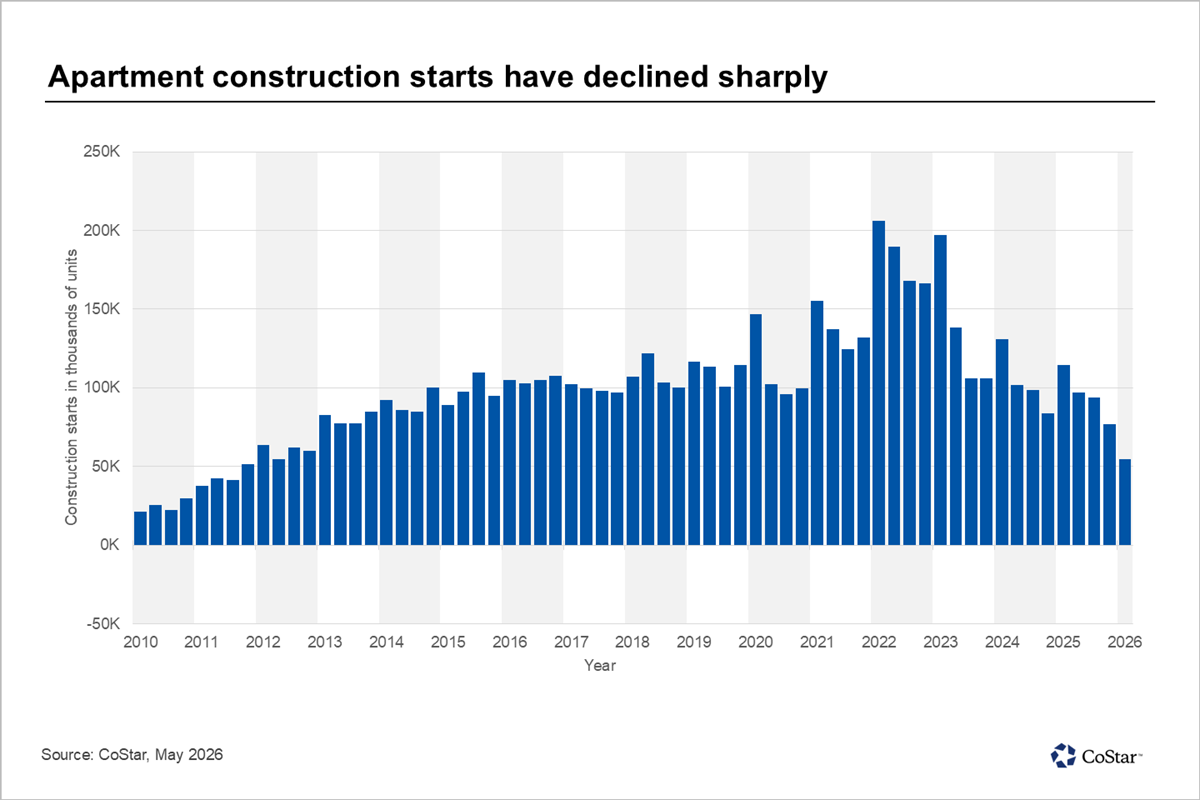

Construction starts fall to lowest level since 2011

Multifamily construction starts have trended downwards since peaking in early 2022.

In the first quarter of 2026, construction starts contracted further, declining to about 55,000 units, representing a 73 percent drop from the development peak reached in early 2022. It was the lowest quarterly total recorded since 2011.

Several factors are contributing to the slowdown, including weaker rent growth, high construction financing costs, and rising development costs.

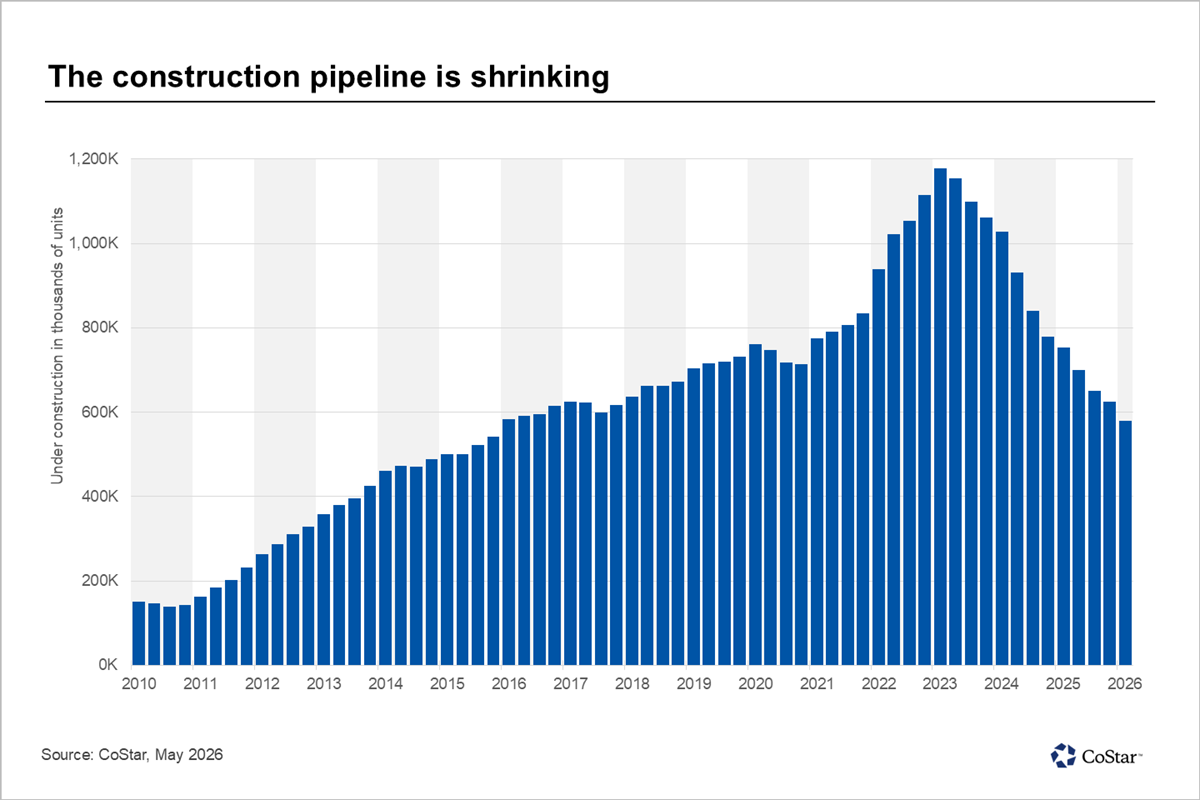

Units under construction continue to decline

With the slowdown in construction starts, the overall development pipeline has also shrunk.

After staying above 1 million units from mid-2022 through early 2024, the number of units under construction has continued to fall. In the first quarter, units under construction totaled 579,000, down more than 50 percent from the peak reached in early 2023.

Current construction activity is now comparable to levels seen during the mid-2010s before the pandemic-era development boom. In early 2016, for example, the total number of units under construction totaled nearly 581,000.

“Developers have pulled back sharply as weaker rent growth and higher financing costs weigh on project feasibility,” said Grant Montgomery, national director of U.S. multifamily analytics at CoStar. “While completions remain elevated for now, the contraction in the construction pipeline points to more balanced supply conditions ahead.”

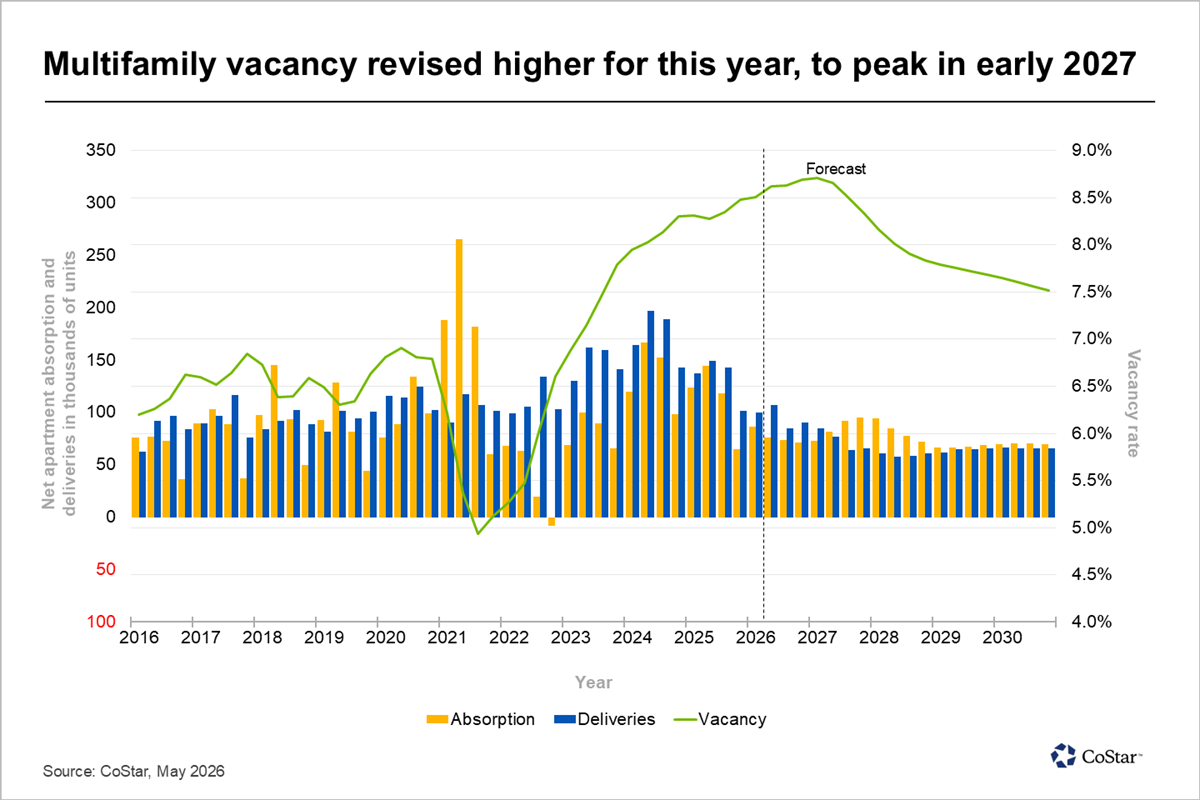

Deliveries remain elevated but are trending lower

Although the development pipeline is shrinking, the market is still absorbing a large volume of recently completed units.

Multifamily deliveries reached a 40-year record in 2024. Since then, deliveries have declined 26 percent over the past year.

And this trend is expected to continue. In 2026, new deliveries are projected to decline 28 percent to 382,000 units. In 2027, deliveries are expected to fall another 24 percent.

Rising vacancy expected to peak in early 2027

Even with the rapid decline in multifamily deliveries, the excess supply created by the development boom sparked during the COVID-19 pandemic continues to linger, driving up the vacancy rate.

Supply is still projected to outpace absorption, or the net change in occupancy.

Vacancy is expected to climb more than previously anticipated, peaking in early 2027. The vacancy rate is projected to reach 8.8 percent by the end of 2026, up from 8.5 percent at the end of 2025. Vacancy is then expected to ease slightly to 8.4 percent by the end of 2027.

Over the longer term, vacancy is expected to decline only modestly during the next five years.

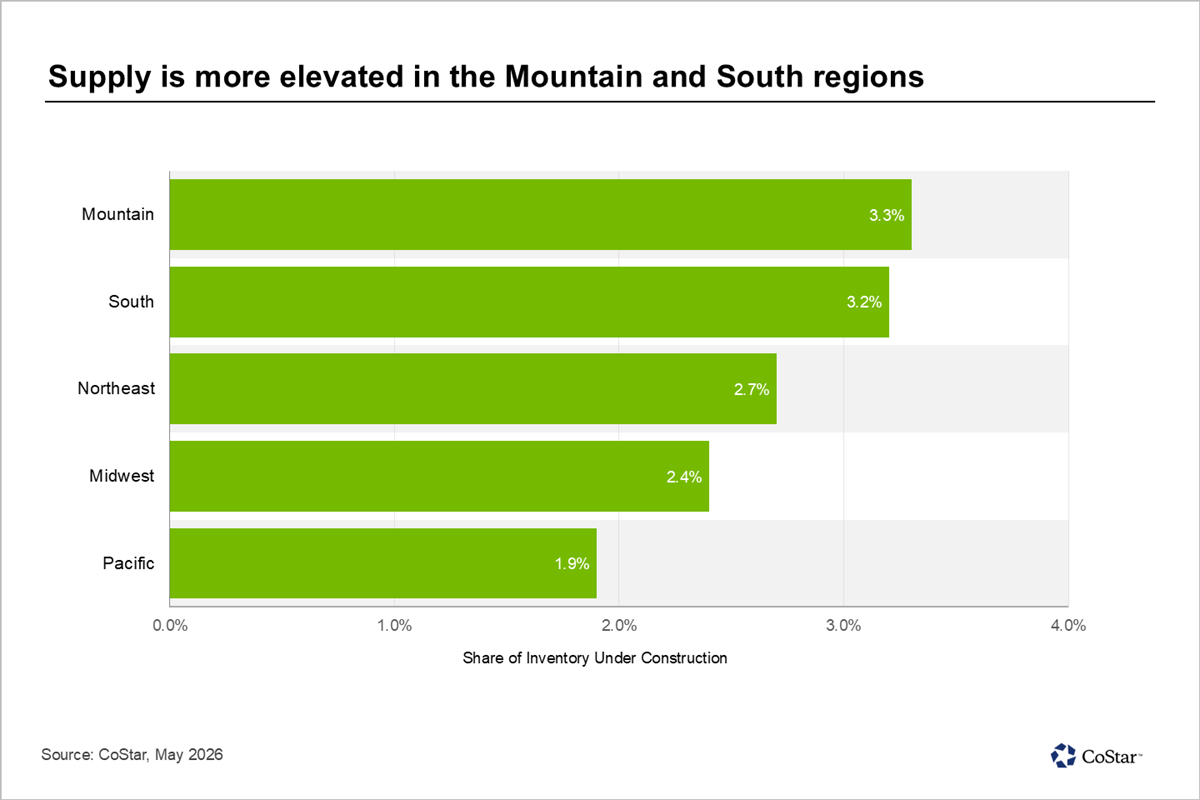

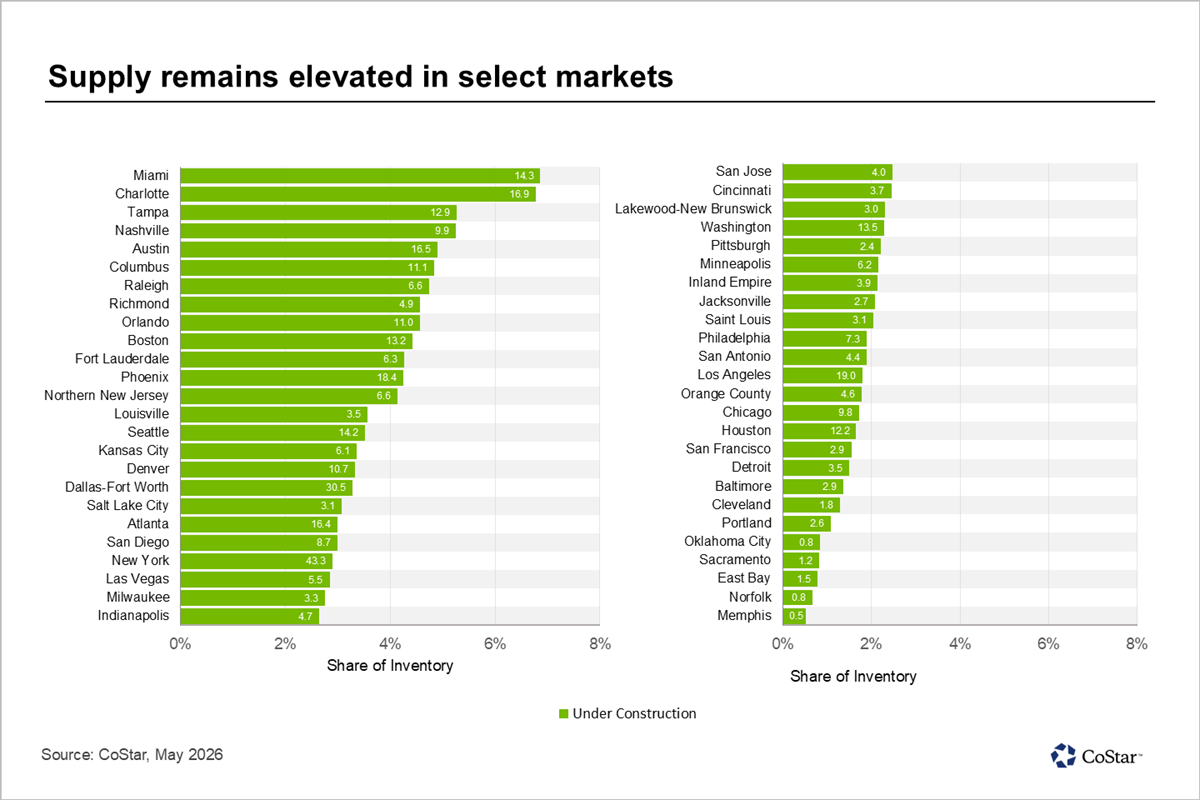

Mountain and South face most active development pipelines

Development pipelines remain uneven across regions.

The Mountain and South regions have the most active development pipelines relative to inventory, at 3.3 percent and 3.2 percent, respectively. The Northeast and Midwest are more constrained at 2.7 percent and 2.4 percent, while the Pacific region has the lowest exposure to new supply at 1.9 percent.

Among individual markets, New York City leads the nation in construction volume with more than 43,000 units under construction. Dallas-Fort Worth follows with about 31,000 units.

Relative to market size, Miami and Charlotte remain among the most active development markets, with more than 6 percent of total inventory currently under construction.

Rent growth outlook softens

With the supply overhang continuing to pose a significant challenge, the rent growth forecast has been revised lower. Annual rent growth is now expected to end the year at 0.5 percent, down from the previous forecast of 0.6 percent.

In addition to ongoing supply pressures, a softer employment outlook is contributing to weaker rent growth expectations.

Over the long term, annual rent growth is projected to average 1.5 percent, below historical norms.

Renter demand faces growing headwinds

Demand for apartments is expected to weaken in the coming years as economic and demographic challenges weigh on household formation and rental demand.

Quarterly absorption is projected to decline to 70,000 units, falling below the five-year pre-pandemic average. At the same time, several economic factors are expected to limit demand growth. Higher energy prices have reduced consumer spending power, while employment growth expectations have been downgraded due to tariff policy, slow labor force growth, and increased productivity.

Lower immigration, which has constrained labor force and employment growth, has also weakened rental demand. Due to these factors, population growth and household formation are projected to remain limited as well.

Together, these factors point to a more challenging environment for renter demand, increasing the risk of weaker multifamily market performance in the years ahead.

Explore more market analysis

Get the latest on the trends shaping the multifamily market: