If you are looking for a way to make some money, investing in a rental property can be a good way to do so. However, it is not as simple as buying a property and then leasing it to a tenant.

Many steps are involved, including the purchasing and financing part. Financing a rental property can be challenging, but it is an achievable and realistic goal for those who come prepared.

- Should I buy a rental property?

- Picking a location and property

- Buying a rental property

- Calculating the return on investment

- Managing the rental property

Should I Buy a Rental Property?

There are a lot of different factors you should consider before you buy a rental property, as it is a big investment. First, consider what you want to gain from owning a rental. This helps you decide and narrow down what kind of property you want. Ask yourself:

- Do you want this as passive income, or will this be your main source of income? What are your financial goals overall, and how does this investment fit in?

- Do you have the skills, time, and readiness to own and manage a property?

- Do you want a property that needs renovations or a move-in-ready property?

Renting out a room can be a low-risk way to test whether being a landlord is right for you before committing to a full rental property. If you’re ready to take the next step, make sure you’re prepared with the financials, research, and plan you’ll need to succeed.

Picking a Location and Property

Now that you have decided to buy a property, it is time to find one. The best way to start is to figure out what you want. First is location; start by looking at the big picture and then at smaller details. When looking at the big picture, you should consider factors like:

- Risk of natural disasters

- Population growth in the area

- Rental rate/vacancy trends

- Crime

- Market prices

- Property taxes

- Rent vs. ownership

Next, you should look more closely at the specific neighborhood and area you want to buy a property in:

- Neighborhood growth

- Nearby amenities

- Walk score, bike score, and sound score

- Nearby education like schools and universities

- Local transportation

- Employment opportunities

When looking at specific properties, you need to decide if you want a property that needs more work or is mostly ready. When considering properties, look at:

- Yard size/potential yard maintenance

- Age and condition of property

- Needed maintenance/repairs

- Curb appeal

- Ages and conditions of major systems, like HVAC

- Ages and conditions of appliances (if included in the sale)

- Additional property amenities, such as a pool, shed, etc.

Once you’ve found a property, you should have inspections done to ensure everything is in decent order before buying the place. Some important inspections are:

- General home

- Electrical system

- Plumbing

- Foundation/Structural

- Roof

- Vents

- House systems, such as HVAC

- Pest

- Mold

You should also consider if you want to do any renovations/installations that could raise the property value. Depending on your location, renters value amenities such as eco-friendly features, granite countertops, walk-in closets, and more.

Financing and Buying a Rental Property

There are a lot of moving components when it comes to financing a rental property. Getting a mortgage is one of the biggest parts; be ready for lenders to scrutinize your finances.

Mortgages

There are many ways to buy an investment property, but keep in mind that financing often comes with higher interest rates and larger down payments than a primary residence. Mortgage options generally fall into two categories: government-backed and conventional.

Government-backed mortgages

You should be familiar with the names Fannie Mae and Freddie Mac as you go through the process. These government-sponsored entities buy most of the mortgage loans (including conventional loans) lenders make, allowing lenders to use that money to make more loans.

For context, Fannie Mae and Freddie Mac set mortgage guidelines—like down payment, credit score, and DTI—so lenders usually mirror those requirements.

Conventional mortgages

Conventional mortgages are the most common type of mortgage. These mortgages come directly from lenders and are not government-backed. Anyone can qualify for these loans if they meet the lender’s standards. There are two types of conventional mortgages:

- Conforming: Conforming loans comply with mortgage loan limits set by the Federal Housing Finance Agency and Fannie Mae and Freddie Mac guidelines. Conforming loans have a maximum dollar limit, which means the house must be near or under that limit. Conforming loans can be easier to qualify for, have lower mortgage rates, lower down payment, and more.

- Non-conforming loans exceed loan limits or are outside Fannie Mae/Freddie Mac underwriting guidelines. These include Jumbo Loans, designed for properties that are more expensive than conforming loan limits. The criteria to get this loan are much stricter, and there might be higher mortgage interest rates.

Loan terms

Common loan terms include 15, 20, and 30 years. Longer terms usually lower your monthly payment, but often come with a higher rate and higher total interest costs.

Interest rate types

Mortgages generally come as fixed-rate (FRM) or adjustable-rate (ARM). A fixed-rate mortgage keeps the same interest rate for the entire loan term.

If you choose an adjustable-rate mortgage (ARM), the interest rate can change over time based on market conditions. This can be beneficial if the initial rate is lower, but it also introduces payment uncertainty because the rate—and your monthly payment—may increase later.

Down payment

Your down payment can affect your mortgage rate—larger down payments often qualify for lower rates. While 20 percent is common, requirements vary by loan type, and lower down payments may require mortgage insurance.

Credit score

Credit score requirements vary by mortgage type. Conventional loans typically require at least 620, but scores around 740 often qualify for better rates. Lenders also review your credit report for red flags.

Debt-to-income ratio (DTI)

Lenders will calculate your debt-to-income ratio to decide if they should loan to you or not. This shows how much of your monthly gross income goes to pay debts. There are two kinds of DTI:

| DTI type | What it measures | How to calculate | Typical target range* |

| Front-end DTI | Share of gross income going to housing costs | (Monthly housing payment ÷ gross monthly income) × 100 | 28%–35% |

| Back-end DTI | Share of gross income going to all monthly debt payments | (Total monthly debt payments ÷ gross monthly income) × 100 | 36%–43% |

*Ranges cited from Experian.

Other factors lenders consider

Lenders may also review your employment and income history, along with your available assets, to assess overall risk. Consistent income can strengthen your application, while liquid assets and cash reserves can show you have a buffer for unexpected expenses or vacancies.

In some cases, property characteristics and marketability—such as property type, condition, or appraisal factors—can also influence loan approval and pricing.

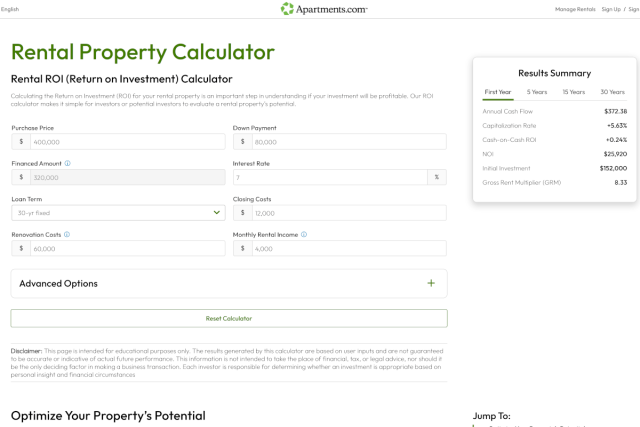

Calculating Return on Investment (ROI)

When you buy a rental property, it’s important to account for expenses and estimate your return on investment. ROI shows how profitable the property could be by measuring profit as a percentage of what you invested. In general, a higher ROI indicates a stronger return.

To calculate your ROI, you will need your cost of investment, monthly expenses, and monthly income and you will use the formula:

- ROI = (investment gain – investment cost) ÷ investment cost

Expenses typically include mortgage, insurance, property taxes, maintenance costs, homeowner’s association fees (if applicable), other costs required to own and operate the property.

A common guideline suggests that 50 percent of your rental income should be set aside for expenses. Regarding maintenance costs, you should estimate about one percent of your yearly property value.

Using the ROI calculator on Apartments.com is easy. Enter your purchase price, down payment, financed amount, interest rate percentages, loan term, closing costs, renovation costs, and monthly rental income.

If you want to get into more detail, you can input advanced options, including monthly recurring expenses and yearly growth percent. The results summary will pull up your returns for the first year, five years, 15 years, and 30 years.

The return on investment rental property calculator gives you several ways to assess your rental property’s value as the results include annual cash flow, capitalization rate, cash-on-cash ROI, net operating income (NOI), initial investment, and gross rent multiplier.

ROI alone doesn’t provide a complete picture of a rental property’s performance, so it’s best to evaluate returns using multiple metrics. A rental property calculator can run these calculations for you in one place.

Calculating rent

Another important part of being profitable is being able to calculate the rent for your property.

There is no perfect formula telling you how much you should charge for rent. You’ll need to understand market demand and trends, analyze comparable properties, consider property condition and amenities, be familiar with the current economy, and budget for maintenance and utilities.

This may feel daunting, but rent comp reports on Apartments.com can help you price your rental with confidence. For a more complete view, pair a rent comp report with a rent analysis report to support an informed decision.

Managing Your Rental Property: DIY vs. Hiring a Property Manager

Figuring out how to manage a rental property is the next step. There are two options: managing your own rental property (called DIY (do it yourself) management) or hiring a property manager.

When trying to decide if you should hire a property management company, you need to weigh the pros and cons of each option to decide what is best for you. If you don’t want to spend any extra money on a property manager, you could opt for DIY management.

If you don’t have the time to manage day-to-day responsibilities, hiring a property manager may be a wise option. Whether you decide to manage the property on your own or hire someone, you still need to have a clear understanding of the landlord's role. While responsibilities may vary, common tasks and frequency include:

| Responsibility area | Common tasks | Typical frequency |

| Managing tenants | Tenant screening; processing applications; scheduling move-ins and move-outs | As needed (during vacancies/turnover) + ongoing tenant communication |

| Maintaining the property | Cleaning; landscaping; repairs and maintenance coordination | Ongoing + seasonal (landscaping) + as needed (repairs) |

| Financial management | Setting rent prices; collecting rent and fees; handling security deposits; managing taxes; tracking income and expenses | Monthly (rent collection, bookkeeping) + as needed (pricing) + annual/seasonal (taxes) |

Laws

Part of owning and managing a rental is understanding the laws involved, from fair housing laws and credit reporting laws to tenant screening laws and eviction laws.

Further, depending on your location, there may be city and state-specific laws that you must follow. Be sure to thoroughly read and research all laws surrounding rental properties, landlords, and tenants. To become well-versed in local regulations, great resources include your city’s website, realtor associations, and non-profit organizations.

FAQs

How can I find tenants for my rental property?

You can find tenants for your rental property by listing on Apartments.com for free. Apartments.com helps your detailed listing reach millions to fill vacancies fast. It is a quick and effortless process; all you have to do is sign up using your email, give your property’s basic details, and upload some photos. Make sure your listing abides with fair housing laws and other local laws to avoid any complications.

Should I invest in short-term or long-term rental properties?

Short-term and long-term rentals offer unique advantages and disadvantages and attract different kinds of tenants. Short-term rentals generally have a greater potential to earn money and a higher tenant turnover.

You might spend more time screening tenants and reviewing applications in addition to having a less stable source of revenue. Long-term leases are a good choice for those who want consistent revenue and a lower turnover rate. This can mean having a lower rent price to compete with other rentals in your area.

What is the 2% rule for an investment property?

The 2 percent rule is a bit of a niche and outdated way to assess the profitability of a rental property. It says if you make 2 percent of the purchase price from rent each month, then you have made a good investment. Do be aware that this rule is rarely used as each property is different, and the market is constantly changing.

How much monthly profit should you make on a rental property?

There isn’t a single “right” monthly profit target because it depends on your market, financing terms, and risk tolerance.

Instead of aiming for one dollar amount, evaluate profitability using a few key metrics—especially monthly cash flow (income minus all expenses and debt), along with cash-on-cash return, cap rate, net operating income, and gross rent multiplier (GRM)—to see whether the property meets your return goals.

This article is not intended as financial advice and should not be construed as such. Before purchasing a rental property, please contact a qualified financial advisor or real estate attorney.