Published on

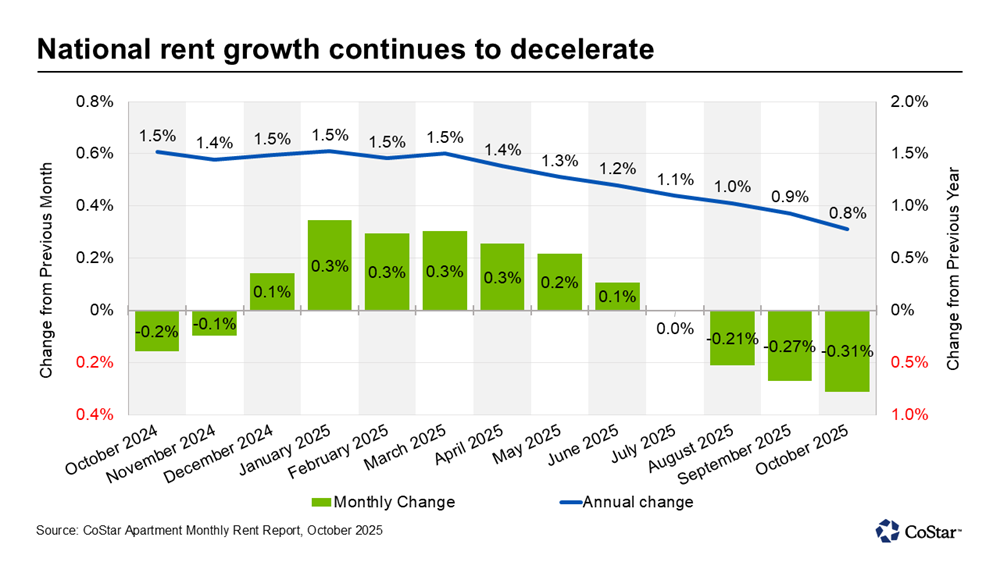

Annual rent growth, which has remained modest since late 2023, slipped to 0.8 percent in October, according to the latest CoStar report. While slowing rent growth is in line with typical seasonal patterns, the degree of this deceleration reflects the challenging conditions currently facing the multifamily market.

The steady deceleration of rent growth continues

The rate of rent growth has nearly halved since this time a year ago, based on the latest revised numbers since October of last year. Rent growth hovered between 1.5 and 1.4 percent from last October through this April.

Currently at 0.8 percent nationwide, annual rent growth has slowed beyond the usual seasonal downturn. Rent growth typically accelerates in spring and begins to slow down by late summer and fall.

October marks the fourth consecutive month of flat or negative monthly rent change and the steepest month-over-month decline for October in over 15 years.

After reaching a 40-year record last year, new supply additions have slowed this year, falling 30 percent, with a total of 495,000 units projected to be added by year’s end. Even though new deliveries have decreased, the huge wave of new supply in recent years is continuing to take a toll on rent growth.

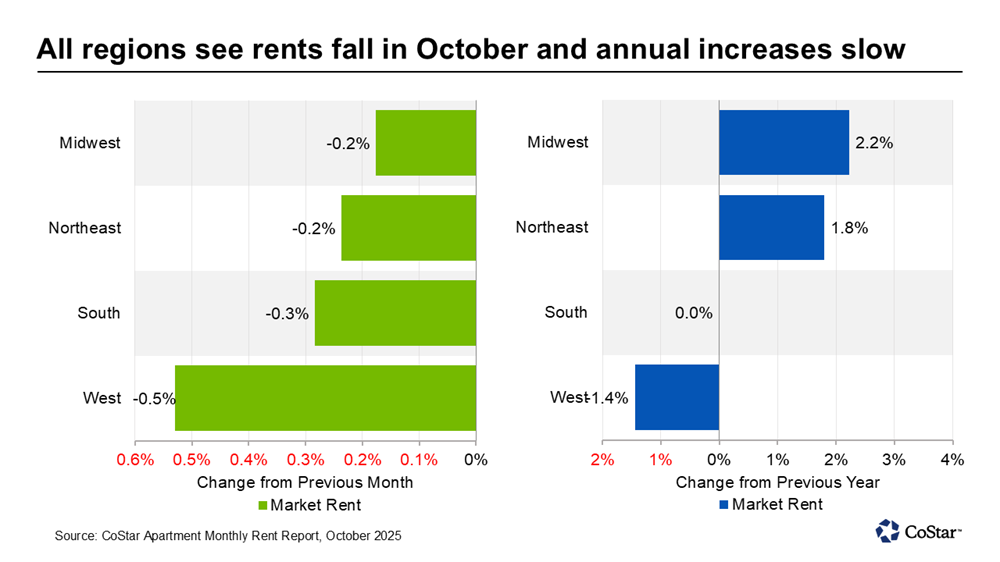

Only Midwest and Northeast regions post rent growth

The Midwest maintains its position at the top of the rent growth charts. The region, which includes top-performing Chicago (3.6 percent rent growth) and Minneapolis (2.3 percent rent growth), posted an average of 2.2 percent annual rent growth.

The Northeast, the other region to outperform the national average, saw rents increase by 1.8 percent year over year.

In contrast, rents remained flat in the South, where rent growth averaged 0 percent. The West, which has fallen behind the rest of the country in recent months, saw rents decline by 1.4 percent.

Even the strong performance of West’s top performers San Francisco and San Jose was insufficient to keep the regional average in the black.

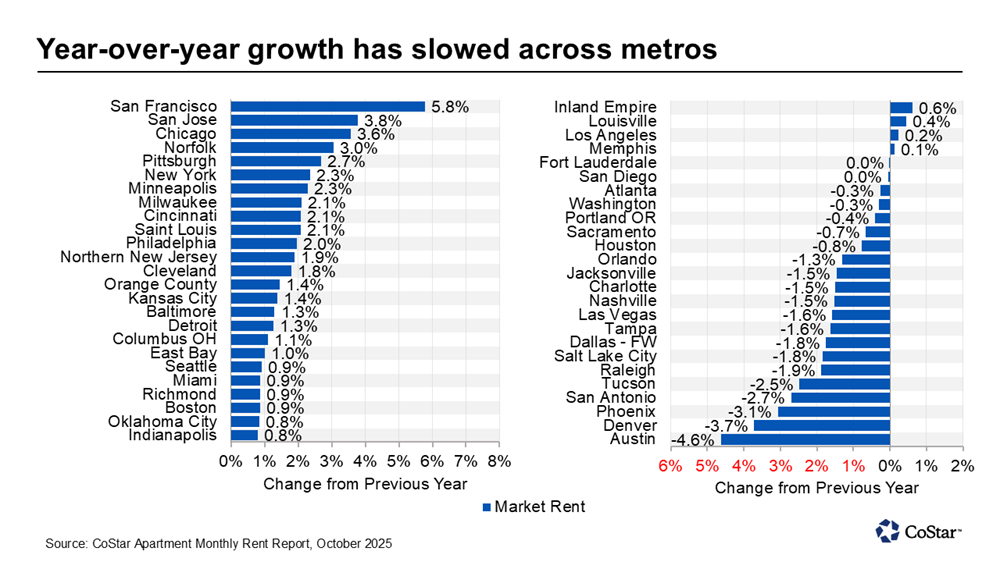

San Francisco again led market-level rent growth charts with an impressive 5.8 percent rent growth, over seven times the national average. The San Jose market came in second with 3.8 percent rent growth.

Rent per square foot in these two markets is also among the highest in the nation.

At the other end of the scale, Austin remains in last place among major multifamily markets, with rent growth of negative 4.6 percent.

The oversupplied Texas capital was joined in the bottom five by Denver, Phoenix, San Antonio, and Tucson. Rents in these markets fell by 3.7 percent, 3.1 percent, 2.7 percent, and 2.5 percent, respectively.

Like Austin, these markets are facing the consequences of rapid development in recent years, which, in the face of insufficient demand, has driven up vacancy rates and turned rent growth negative.

Explore more multifamily insights

For more analysis of the multifamily market, watch the mid-year outlook with CoStar’s Connor Devereux:

And for a glimpse into the future, check out Apartments.com’s 11 predictions for the year ahead, including the latest projections about rent growth, new supply, and concession use in 2026.